Strategic Context: Global Capital Mobility and the Policy Risk Hedge

Entering the second quarter of 2026, the global macro-economic environment remains defined by a significant flight toward high-quality U.S. assets. According to the IMF World Economic Outlook (2025), the United States continues to provide the most robust environment for capital preservation and long-term growth. However, for high-net-worth families, the challenge has shifted from asset selection to residency selection.

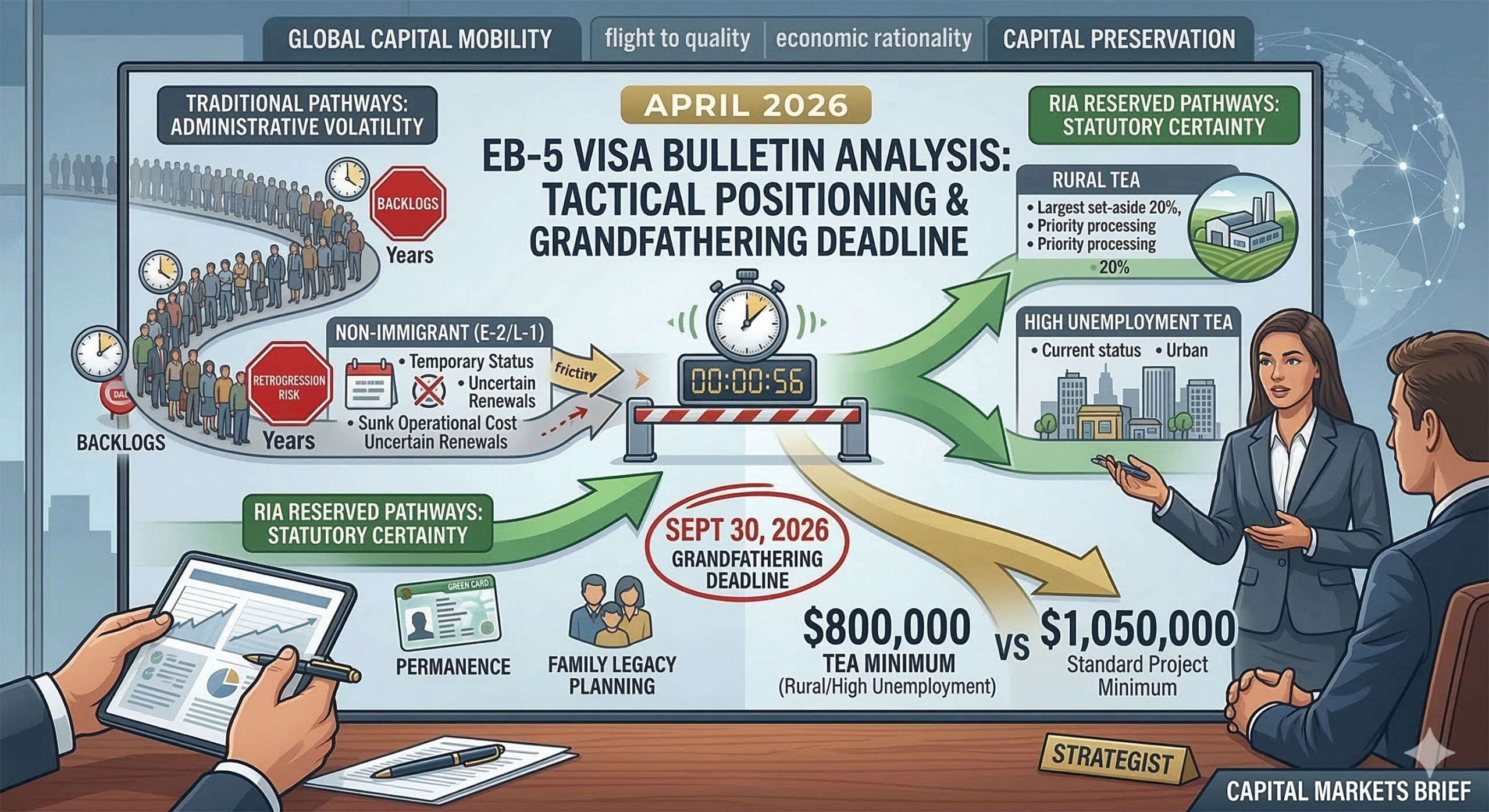

The release of the U.S. Department of State April 2026 Visa Bulletin (link here) underscores a widening efficiency gap between traditional employment-based visas and the statutory “fast lanes” established by current law. As noted by the Congressional Research Service (2024), administrative bottlenecks in standard immigrant categories have increased the “uncertainty tax” for international professionals. In this climate, residency is being re-evaluated not as a mere immigration status, but as a strategic hedge against geopolitical volatility and administrative stasis.

Program Breakdown: The April 2026 Status and Statutory Certainty

The April 2026 Visa Bulletin confirms that the EB-5 program’s “Reserved” categories remain the only operational bypass for backlogged nationalities.

What is Statutorily Confirmed:

- Reserved Category Currency: The April Bulletin indicates that the 20% Rural Area, 10% High Unemployment, and 2% Infrastructure set-asides remain “Current” for all countries. This status allows for immediate filing of the I-526E petition, bypassing the multi-year retrogression observed in the unreserved categories.

- The Sept 30, 2026 Grandfathering Deadline: Under the EB-5 Reform and Integrity Act of 2022 (RIA), Section 103 provides a statutory “grandfathering” protection. Any investor who files a valid petition on or before September 30, 2026, is legally insulated from future program lapses or legislative sunsets.

- Investment Minimums: The threshold remains fixed at $800,000 for Targeted Employment Areas (TEAs)—including Rural and High Unemployment areas—and $1,050,000 for standard projects.

Economic and Strategic Comparison: Non-Immigrant Risk vs. EB-5 Permanency

For many global entrepreneurs, the choice often involves comparing the E-2 (Treaty Investor) or L-1 (Intracompany Transferee) visas against the EB-5. Evaluating these through the lens of economic rationality reveals a significant difference in long-term capital efficiency.

Non-Immigrant Pathways (E-2/L-1):

- Capital Requirement: $200k–$400k (Operational/Sunk Cost)

- Status: Temporary/Discretionary (Subject to renewal)

- Statutory Basis: INA §101(a)(15)

- Risk Profile: High exposure to executive-level policy shifts and consular discretion.

EB-5 Immigrant Investor (Rural TEA):

- Capital Requirement: $800,000 (At-risk investment/Repayable)

- Status: Permanent (Statutory Green Card)

- Statutory Basis: EB-5 Reform and Integrity Act of 2022

- Risk Profile: Business risk mitigated by RIA fund administration requirements and statutory grandfathering.

While the EB-5 requires higher upfront capital, the “return on residency”—measured in the elimination of renewal costs, legal fees, and the “lock-in” effect of employer-sponsored status—often makes it the more economically sound allocation over a five-year horizon.

Tax and Regulatory Exposure: The Worldwide Income Threshold

Investors must prepare for the fiscal implications of Lawful Permanent Residency (LPR). Under the IRS framework, U.S. residents are taxed on their worldwide income, regardless of its source.

Key Compliance Obligations:

- FBAR & FATCA: Mandatory reporting of all foreign financial accounts (FinCEN Form 114) and specified assets (Form 8938).

- Basis Optimization: Pre-immigration tax planning is essential to optimize the tax “basis” of non-U.S. assets before residency is established.

- Exit Tax Awareness: Investors maintaining LPR status for 8 of the last 15 years may be subject to the mark-to-market exit tax upon expatriation.

Market Sentiment: The “Window of Currency”

In institutional circles, the sentiment regarding the April 2026 Bulletin is one of “cautious urgency.” This is not driven by marketing, but by the mathematical reality of visa consumption.

Confirmed vs. Market Speculation:

- Confirmed: The $800,000 threshold and Rural priority processing are currently anchored in federal law.

- Market Opinion: Analysts suggest that the High Unemployment (Urban TEA) category may face retrogression risk by late 2026 due to high filing volumes. Consequently, Rural projects—receiving the largest set-aside (20%) and priority adjudication—are viewed by family offices as the most resilient entry point.

Why EB-5 Remains Structurally Positioned

The EB-5 program remains the premier residency asset for three reasons:

- Concurrent Filing: Investors currently in the U.S. can file Form I-485 simultaneously with their I-526E, granting immediate work and travel rights.

- Statutory Bypass: The set-aside categories offer the only reliable bypass to the multi-decade backlogs for Indian and Chinese nationals.

- Institutional Oversight: The RIA mandates independent third-party fund administration, aligning EB-5 capital with private equity transparency standards.

Final Strategic Conclusion

The April 2026 Visa Bulletin confirms that the “window of currency” for EB-5 set-asides is still open, but the September 30, 2026 grandfathering deadline represents a hard stop for statutory protection. For investors, the focus must be on disciplined analysis: acting while categories are “Current” and before the programmatic sunset to insulate residency from future policy risk.

For families evaluating long-term U.S. positioning and seeking a structural resolution to global volatility:

[Click here to see our currently available EB-5 projects.]

Citation List

- U.S. Department of State (2026). Visa Bulletin for April 2026.

- EB-5 Reform and Integrity Act of 2022 (RIA). Public Law 117-103.

- USCIS Policy Manual (2025). Volume 6, Part G: Investors.

- Congressional Research Service (2024). The EB-5 Immigrant Investor Program: Background and Policy.

- Internal Revenue Service (2025). Publication 519: U.S. Tax Guide for Aliens.

- IMF World Economic Outlook (2025). Global Economic Growth Projections.

The “Current” status for EB-5 Reserved categories—specifically Rural (20%), High Unemployment (10%), and Infrastructure (2%)—exists because these set-asides were established as a new, separate visa pool under the EB-5 Reform and Integrity Act of 2022 (RIA). While traditional EB-2 and EB-3 employment categories face decade-long per-country caps, these RIA-specific pools have not yet reached capacity. This allows investors to bypass historical retrogression and proceed with immediate petition filing.

Section 103 of the RIA provides a statutory “grandfathering” protection for any investor who files a valid Form I-526E on or before September 30, 2026. This rule mandates that USCIS must continue processing your petition even if the Regional Center program faces a future legislative sunset or political lapse. For investors, this creates a definitive window of legal certainty, insulating your $800,000 capital from future regulatory shifts.

Yes. Because the April 2026 Bulletin shows the Reserved EB-5 categories as “Current,” investors lawfully present in the U.S. can file for Adjustment of Status (Form I-485) simultaneously with their investor petition. This grants you immediate access to a “combo card” (Employment Authorization and Advance Parole), effectively decoupling your residency status from your employer and eliminating the risk of H-1B “lock-in” or supplemental renewal fees.

While both require an $800,000 investment, Rural projects are statutorily mandated to receive Priority Processing by USCIS. Furthermore, Rural projects receive the largest portion of the set-aside visa pool (20% vs. 10% for Urban TEAs). As filing volumes increase toward late 2026, market analysts expect Urban TEA projects to face a higher risk of retrogression, making Rural projects the more resilient choice for minimizing wait times.

Attaining Lawful Permanent Residency (LPR) triggers the IRS Worldwide Income Taxation framework, meaning you will be taxed on your global earnings regardless of the source. Investors must also comply with FBAR (FinCEN Form 114) and FATCA reporting for all foreign financial accounts. To manage this, it is critical to engage in pre-immigration tax planning—such as adjusting the “basis” of your international assets—before residency is officially established.